NZME, the parent company of 13 New Zealand radio stations and the New Zealand Herald, has postponed its annual shareholders meeting until 3rd June.

It was originally scheduled to be held tomorrow, 29th April.

The postponement comes as a result of multimillionaire James Grenon making a bid for board control after buying almost 10% of the company’s shares in March. The company released details of his board director nomination letter in early March, saying:

NZME advises that it has received a letter from James (Jim) Grenon… which contains a proposal to remove all of the current directors of NZME and nominations for the appointment of four new directors to the NZME Board, to be voted on at the upcoming Annual Shareholders’ Meeting. The draft explanatory notes to Mr Grenon and JTG’s letter indicate that it is intended that the four proposed nominee directors would choose a fifth director from the existing NZME Board…

Mr Grenon and JTG’s letter states that they have discussed in confidence these proposals with some of NZME’s largest shareholders, who hold approximately 37% of NZME’s shares. Mr Grenon and JTG’s letter states that those shareholders have indicated to them their support for these proposals… Mr Grenon and JTG’s letter does not identify the other shareholders with whom they state they have spoken…

The directors nominated by Grenon are listed in a NZ Stock Exchange notice from 12th March. Mr Grenon is one of the 6 nominees. His letter to the NZME board explaining the reasons for his bid was released to the Stock Exchange on 21st March and can be read here. His complaints about the current board are:

1) The combined operational performance of the two core businesses has been mediocre, to sliding, for the past 8 years, despite a temporary period of COVID-era gains.

2) I believe the value of the NZME stock is currently driven primarily by two things. One is the stand-alone value of OneRoof, which many seem to think is $0.50 per share or more, and the other is the dividends (which are also somewhat of a proxy for the success of the operations). The disclosure on these two critical elements is, in my opinion, lacking or even misleading.

3) Public disclosure is weak, with a slant that I interpret as supporting the status quo. Just finding the disclosure is my first complaint since it is not even well organized on the website.

4) There has been a consistent pattern of over promising and under delivering since COVID.

5) Recognizing the Evolution of Media – Cost Discipline.

6) Journalism.

7) The Board is now Financially Aligned.

Point 6, which has worried onlookers and the NZ journalism union, has raised fears that Grenon, who moved to New Zealand from Canada in 2012, supports right wing political views and may seek to interfere with the independence of the company’s newsrooms.

In his eleven page letter to shareholders, Gregon addresses point 6 saying he wants to lift journalistic standards. “My intention is that more quality content should be produced, not less. This is needed to attract new subscribers.” He goes on to quote a study showing public trust in the NZ Herald.

Gregon acknowledges the strong performance of the comapny’s Audio Division, saying: “On a more positive note, I applaud the progress NZME has made within its Audio segment with industry leading audience ratings.”

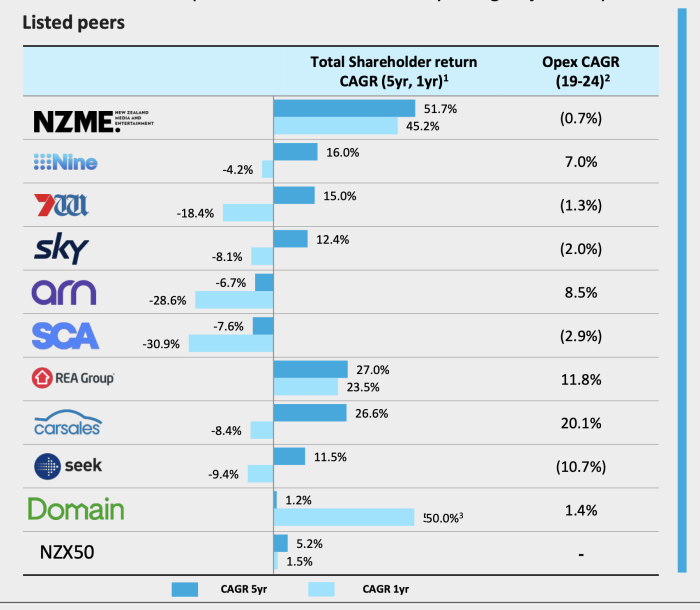

The board has written to shareholders challenging some of Grenon’s claims, saying the company’s compound annual growth rate (CAGR) has remained strong and is outperforming the growth of other Australian and New Zealand media companies.

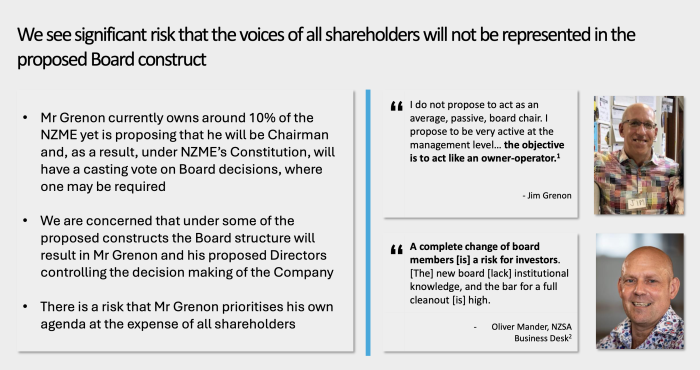

It also outlines what the current board sees as the risks of shareholders voting for Grenon’s nominees.

Meanwhile, the NZ Takeovers Panel has begun an inquiry into whether Grenon’s links with other shareholders constitutes an unauthorised “acssociation” between various parties to the proposed action:

On the basis of the information available to the Panel, the Panel considers that there is reasonable possibility that the parties were associates and therefore certain share acquisitions by Mr Grenon may not have been in compliance with rule 6(1)(a) of the Takeovers Code.