Last week’s GfK Survey 6 was remarkable in many ways, mainly due to the impact of the Coronavirus.

Long established listening patterns, underpinned by the daily commute, were significantly altered as large numbers of workers and students stayed home.

In the two biggest markets, Sydney and Melbourne there was a larger than anticipated shift to AM talk with most FM music stations shedding audience.

But hidden in the numbers was another story of radio “share loss” that even Ashley & Martin would struggle to cover with a rug.

When we added up the audience share figures for each surveyed station in each of the five metro markets, none of them add up to 100 percent.

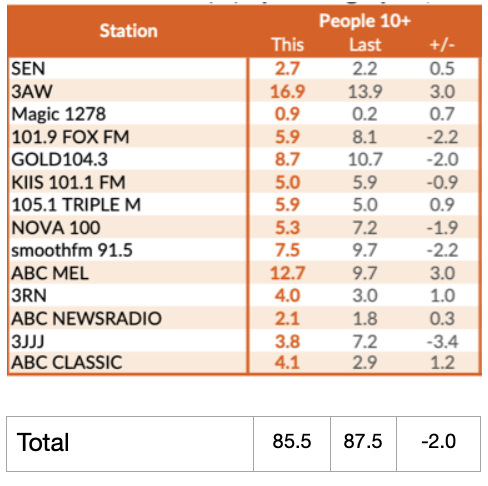

In Melbourne, for example, the total of station shares in Survey 2, 2020 in April added up to just 87.5 per cent. By Survey 6 last week, that number had eroded to 85.5. The bottom line is that 14.5 percent of Melbourne’s available audience does not listen to the stations listed in the GfK diaries handed to those surveyed.

In Sydney, the gap is even wider with close to 15 percent finding “other” audio sources more apealing than surveyed stations.

Brisbane is the only market where the total share incresed since Survey 2.

GfK’s Media Measurement Director, ANZ, Deb Hishon explains, “The gap in the listening is listening that is attributed to Other AM, Other FM and Digital Radio (for the Digital Only stations and Other Digital, as the digital simulcast listening is contained in the reported share numbers for the AM and FM stations) – there are no other audio sources included in the survey.”

Although “other stations” whether AM, FM or Digital are not listed in the Diary, survey respondants can manually insert them. Niether GfK or their client, CRA, is keen to disclose exactly which stations are part of the “others” list and even less keen to reveal what kind of share they might individually command – mainly because they don’t contribute to the cost of the surveys.

Some obsevers contend that, in Sydney, for example, the more popular community broadcasters such as 2ser and Fine Music, as well as commercial stations such as 2SM (which opted out of surveys many years ago) and market fringe stations such as The Edge in Penrith and C91.3 in Campbelltown are part of that mix.

Ms Hishon doesn’t feel that the missing shares are particularly significant, “When we look at the share percentage of ‘other’ across the markets, or the total number that you are referring to, the levels are all within results that we have seen in previous surveys. The same is said if we look at the Average Audience numbers, all markets are within normal fluctuations.”

Peter Saxon

Subscribe to the radioinfo flash briefing podcast on these platforms: Acast, Apple iTunes Podcasts, Podtail, Spotify, Google Podcasts, TuneIn, or wherever you get your podcasts.

I have mentioned this elsewhere on this site about the share of "other" services. It has grown from 2% in the 1970s to about 15-16% today. We don't know about the contributions made by community radio, streaming and commercial stations such as 2SM. For the latter there must be some other research that is used by the sales department in order to sell advertising time.

On the 29th September 2020, I listened to the 'Facebook' post by 2SM's Marcus Paul speaking to caller 'Stephanie' who were discussing the latest Gfk ratings, https://www.facebook.com/marcuspaulradio/videos/the-famous-stephanie/829310454526175/?__so__=permalink&__rv__=related_videos (copy from "https" to "related_videos" and paste in browser) and other issues such as the changes in the "Sydney share movement", that it costs $150000 for participating in the Gfk survey, as well as the 'missing' 15-16% .

Apart from the missing 15%-16%/'other stations', more research is needed to explain the anomaly between 2GB's high ratings and the "movements" statistic, given that Ben Fordham has contributed five months weighting of the figures for an overall rating of 14%.

I disagree with caller 'Stephanie' when she remarked the anomaly of Ben Fordham rating10% during drive, yet rated higher at breakfast at 17% (overall rating 14%) when Ben hosted breakfast. The same could be said for former presenters substituting for Alan Jones including Steve Price, Chris Smith and Jason Morrison. For the latter, Jason Morrison hosted 2UE breakfast and did not rate the same as when he was at 2GB.

The success of the breakfast program at 2GB has been generated by Alan Jones. It could well be said that Alan Jones has generated 'goodwill' over the 35 years. Looking at Marcus Paul's facebook page, he is also generating goodwill.

The next two surveys for 2020 may indicate whether the ratings at 2GB are sustained. The "Sydney share movement" may not be an indicator of where listeners have changed their listening habits. To illustrate, if 2GB's ratings are reduced by 2% in the next survey, how does one account for the 2%? Do all the 2% go to 2BL (702ABC) or RN or 'other 15%-16%' which includes 2SM and community radio? Alternatively do listeners go to music stations?

In sum, more research is needed in the missing/'other 15%-16% together with the share movement statistics.

Thank you,

Anthony of critical Belfield

If you think those 'other' shares are interesting, then check the Gold Coast GFK survey! Most of the Brisbane commercial stations are listed there. Imagine the size of the 'other' category if they weren't.

Personally I love to listening Edge, FBI and 2SER and Fine Music in Sydney...